Robert Hughes

The final January results from the University of Michigan Surveys of Consumers show overall consumer sentiment fell for the sixth time in the last nine months. The recent declines were largely a result of Covid.

Overall consumer sentiment decreased to 67.2 in January, down from 70.6 in December (see top of first chart), a 4.8 percent fall. From a year ago, the index is down 14.9 percent.

The current-economic-conditions index dropped to 72.0 from 74.2 in December (see middle of first chart). That is a 3.0 percent decline and leaves the index with a 17.0 percent decrease from January 2020.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — posted the largest decline, falling 4.2 points or 6.1 percent for the month, to 64.1 (see bottom of first chart). All three measures are at least 25 percent below their 2018 – 2019 averages.

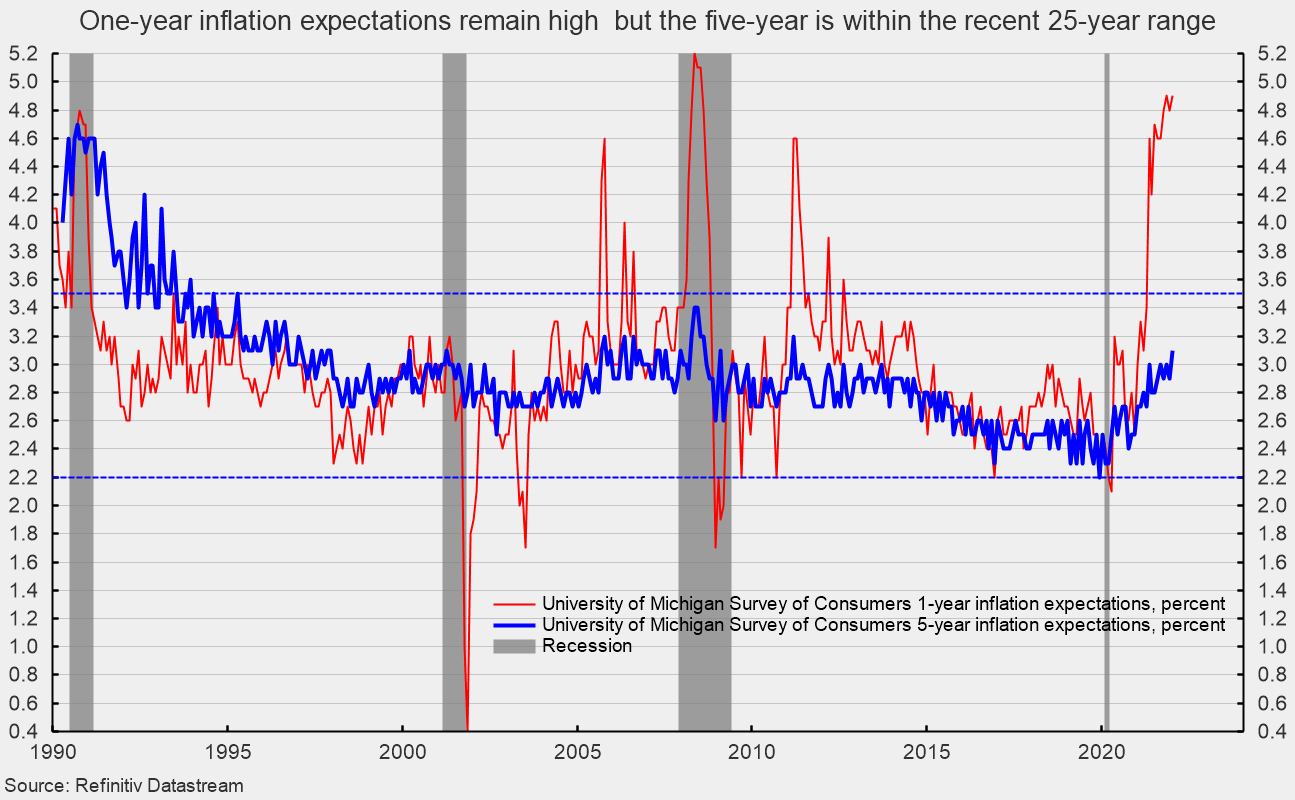

After Covid, the next most influential driver recently has been inflation. Consumer 1-year inflation expectations ticked back up to 4.9 percent, matching the multiyear high from November. Before November, the next highest reading came in July 2008 with a 5.1 percent expectation (see second chart). Though the 1-year expectation is quite elevated, the 5-year expectation has risen far less, coming in at 3.1 percent, up from 2.9 percent in December and a low of 2.2 in December 2019. The most recent result is still within the 25-year range of 2.2 percent to 3.5 percent (see second chart).

The weaker readings in consumer sentiment reflect the one-two punch of the waves of new Covid cases and the sticker shock of higher consumer prices. However, the most recent surge in new Covid cases may be easing already and there are some early signs of easing supply-chain challenges in some areas.

Furthermore, the Federal Reserve is moving to hike interest rates, likely starting in March, and is planning on taking actions to reduce its holding of fixed income securities. These measures should lead to higher short-term and long-term interest rates, thereby reducing demand and eventually loosening the labor market, all of which should ease upward pressure on prices.

The outlook is for continued economic growth, but history suggests that the risk of policy mistakes rises during Fed tightening cycles. Additionally, 2022 is a Congressional election year. Intensely bitter partisanship and a deeply divided populace could lead to turmoil as confidence in election results are coming under constant attack. Contested results around the country could easily lead to government paralysis, testing the durability of democracy and the union itself.

Courtesy: (AIER)