Robert Hughes

Initial claims for regular state unemployment insurance ticked up by 11,000 for the week ending March 5, coming in at 227,000 (see first chart). That is the second increase in the last seven weeks and slightly above the January and February average of 212,000 prior to the lockdowns. By long-term historical comparison, initial claims remain very low.

The four-week average rose in the latest week following four consecutive declines, coming in at 231,250, a rise of just 500. The four-week average appears to be settling into a flat trend, just above the pre-pandemic level. Weekly initial claims data continue to suggest the labor market remains very tight. However, disruptions to the global economy due to the Russian invasion of Ukraine and the impending start of a Fed tightening cycle may cause volatility to economic activity in coming months.

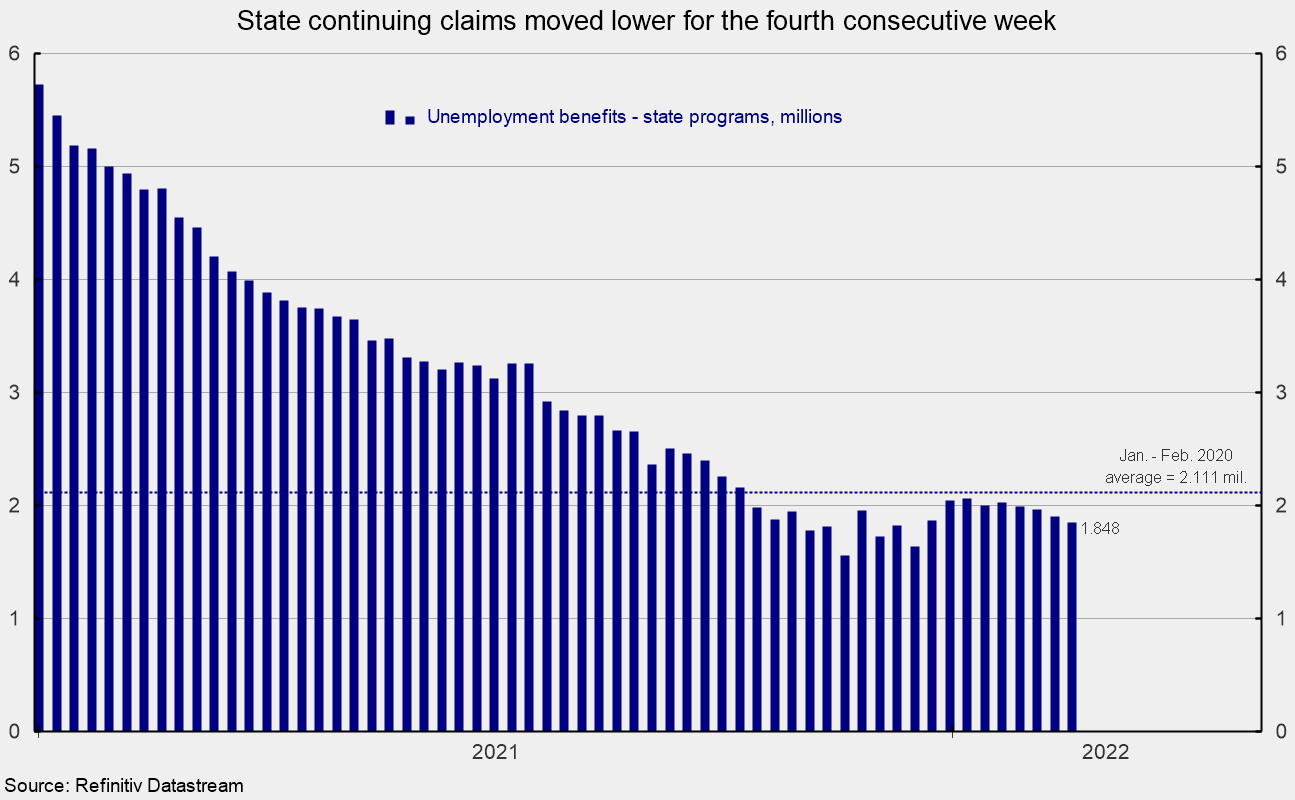

The number of ongoing claims for state unemployment programs totaled 1.848 million for the week ending February 19, a drop of 58,402 from the prior week (see second chart). State continuing claims have declined for four consecutive weeks and remain below their pre-pandemic level of 2.111 million (see second chart).

Continuing claims in all federal programs totaled just 61,089 for the week ending February 19, a drop of 3,857. For January and February 2020, the average for Federal continuing claims was 34,174. Though the current numbers are above the pre-pandemic average, they are just a fraction of the 16.6 million peak and largely reflect the end of the emergency Pandemic Unemployment Assistance program and the Pandemic Emergency UC program.

The latest results for the combined Federal and state programs put the total number of people claiming benefits in all unemployment programs at 1.909 million for the week ended February 19, a drop of 62,259 from the prior week. The latest result is the second week in a row below 2 million.

Despite some volatility over the last few weeks, initial claims remain at an extremely low level by historical comparison. The overall low level of claims combined with the high number of open jobs suggest the labor market remains very tight.

Continuing labor shortages, along with materials shortages and logistical issues, are likely to continue to slow the recovery in production across the economy and sustain upward pressure on prices. In addition, geopolitical and global economic turmoil as a result of the Russian invasion of Ukraine has had a dramatic impact on capital and commodity markets, launching a new wave of disruptions to businesses. Furthermore, an impending new Fed tightening cycle will further weigh on economic activity. The outlook has become highly uncertain.

Courtesy: (AIER)