Robert Hughes

The Consumer Confidence Index from The Conference Board fell in January but remains at a historically favorable level overall. The composite index decreased 1.4 points or 1.2 percent to 113.8 (see first chart). From a year ago, the index is up 30.7 percent.

The decline in the composite index was driven by the expectations component. The expectations component lost 4.6 points, taking it to 90.8 while the present-situation component increased 3.4 points to 148.2 (see first chart). The total index and both components remain well above typical recession lows but also remain somewhat below record highs.

Within the expectations index, expected business conditions, employment conditions, and expected income all fell slightly though buying plans for autos, homes, and major appliances all ticked up slightly. For the present situation index, current business conditions improved while employment conditions weakened slightly.

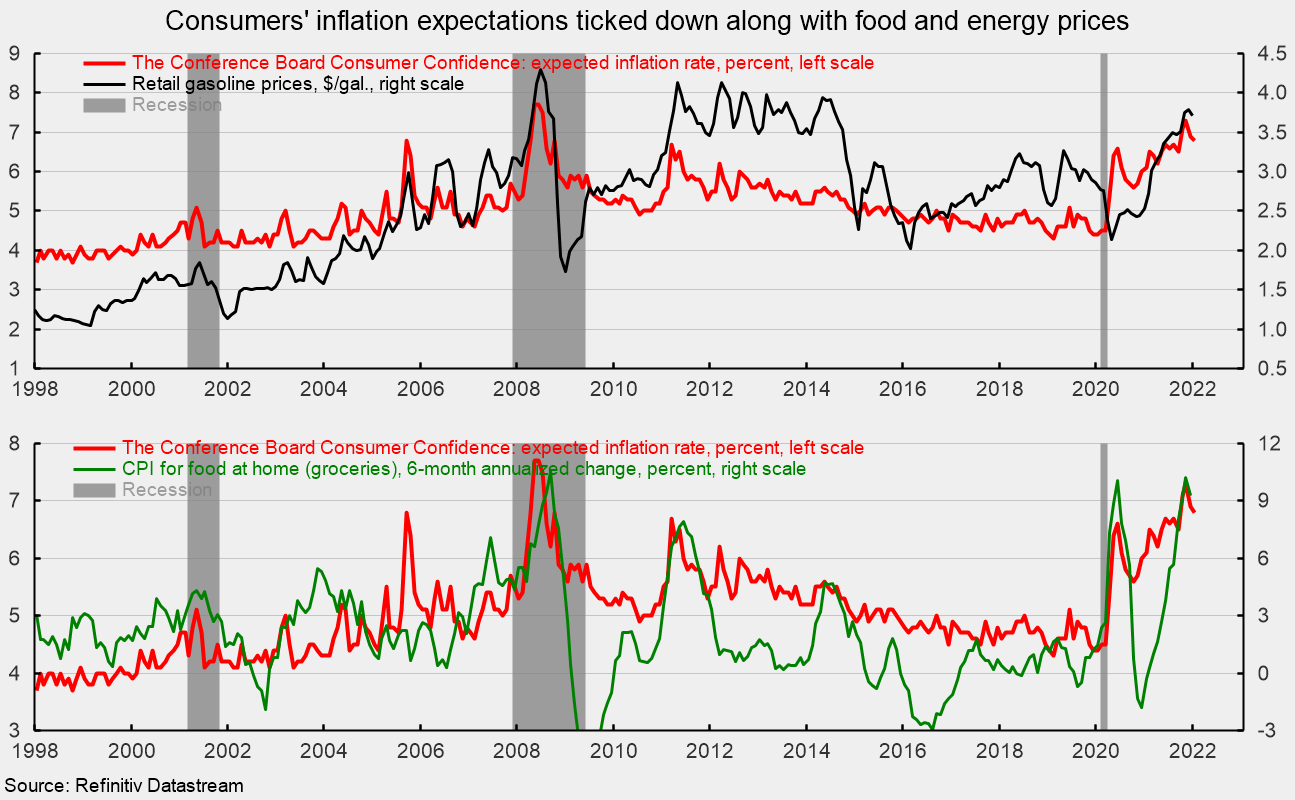

Inflation expectations fell to 6.8 percent in January, down from 6.9 in December and a recent high of 7.3 percent in November; expectations were 4.4 percent in January 2020 (see second chart). The modest easing in consumers’ inflation expectations are consistent with the moderate easing in price increases for gasoline and grocery prices, two of the most frequently purchased items for consumers (see second chart).

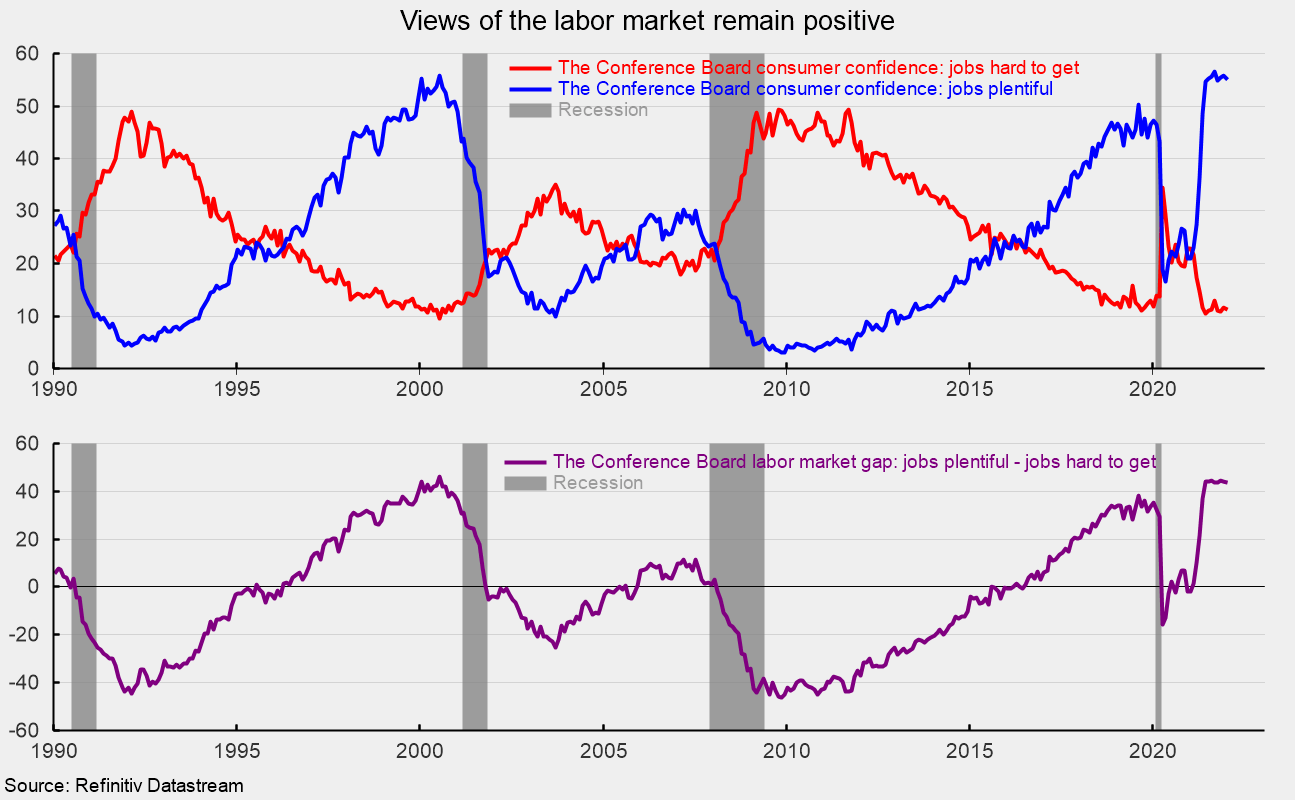

Despite two months of pullback, inflation views have worsened significantly since the start of the pandemic. This stands in sharp contrast to consumers’ views of the labor market which remain a strong support for overall consumer confidence. Current views for the labor market saw the jobs hard to get index ease slightly, falling points to 11.3 (see top of third chart) while the jobs plentiful index fell 0.8 points to 55.1 (see top of third chart) resulting in a 0.4-point decline in the net to a still-strong 43.8. A net above 40 is considered strong by historical comparison (see bottom of the third chart).

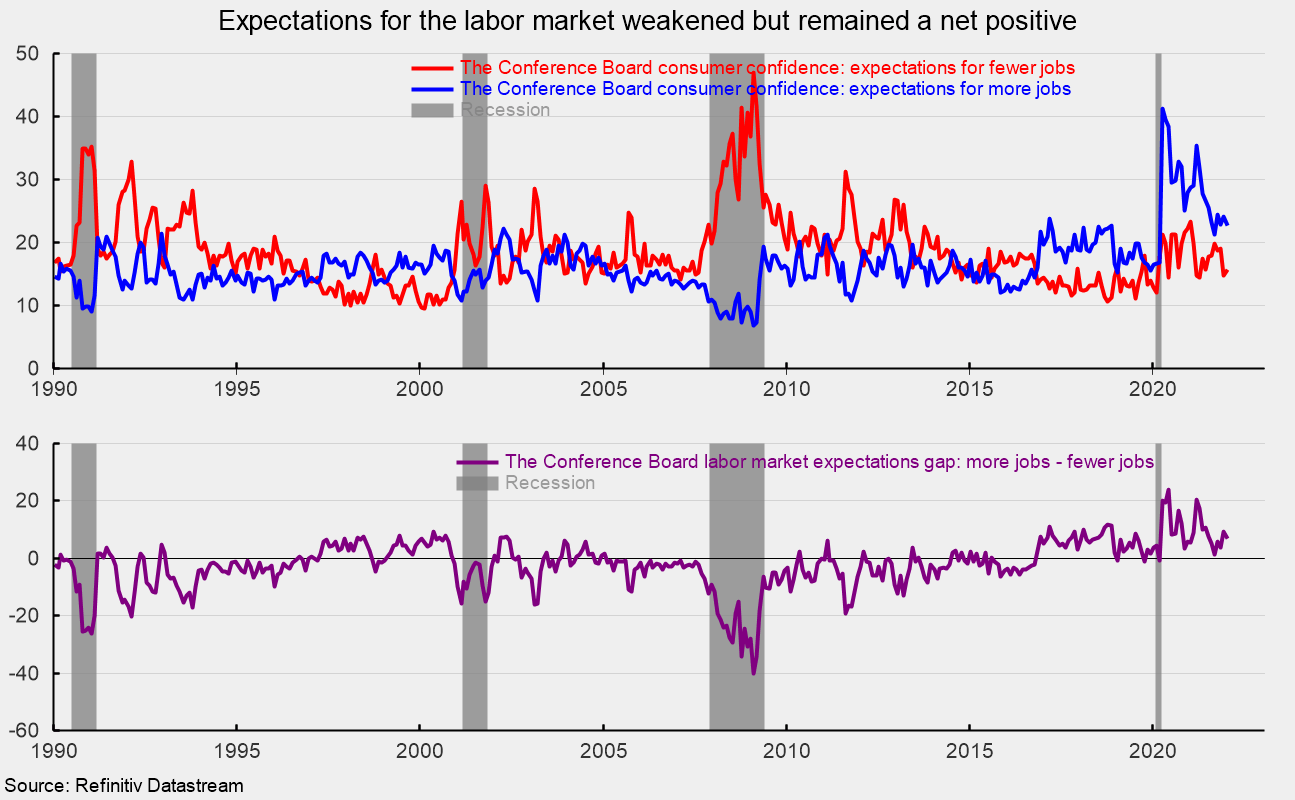

The outlook for the jobs market also weakened in January as the expectations for more jobs index fell 1.5 points to 22.7 (see top of fourth chart) while the expectations for fewer jobs index rose by 1.0 point to 15.7 (see top of fourth chart) putting the net down 2.5 points to 7.0. Still, net positive readings are a favorable result (see bottom of fourth chart).

The outlook for the economy is for continued expansion. However, ongoing shortages of materials, labor difficulties, and logistical problems are sustaining upward pressure on prices (though there may be some early signs of progress on boosting production) and weighing on consumers’ attitudes. A strong labor market offsets the negative views of inflation, resulting in generally moderate consumer confidence.

Courtesy: (AIER)